What Exactly Is a Lis Pendens?

Source: Texas Signals — aggregate county data.

Let's start with the Latin, because it's actually helpful here. "Lis pendens" literally translates to "litigation pending." In real estate, a lis pendens is a public notice filed with the county clerk that says: there is an active lawsuit involving this specific property.

That's it. It's not a lien. It's not a foreclosure. It's not a judgment. It's a warning flag — a legal breadcrumb that tells anyone searching property records that this property is tangled up in some kind of legal dispute.

Now here's why investors care: in Texas, the most common reason a lis pendens gets filed against a residential property is because a lender has initiated foreclosure proceedings. The bank is suing the borrower, and the lis pendens puts the world on notice.

Why Does a Lis Pendens Get Filed?

There are several reasons a lis pendens might show up on a property's record:

1.Mortgage default / foreclosure — By far the most common. The lender is suing to recover the property because the borrower stopped making payments. In Texas, this happens through both judicial and non-judicial processes, though non-judicial (trustee sale) is more common for residential.

2.Divorce proceedings — When a married couple splits and can't agree on what happens to the house, one party may file a lis pendens to prevent the other from selling it during the divorce.

3.Contract disputes — A buyer and seller have a signed purchase agreement, the seller tries to back out, and the buyer files a lis pendens to cloud the title and prevent the seller from selling to someone else.

4.Boundary or ownership disputes — Neighbors disagreeing about property lines, or competing claims to ownership.

5.Mechanic's liens escalating to lawsuits — A contractor who wasn't paid may escalate from a mechanic's lien to a full lawsuit with a lis pendens.

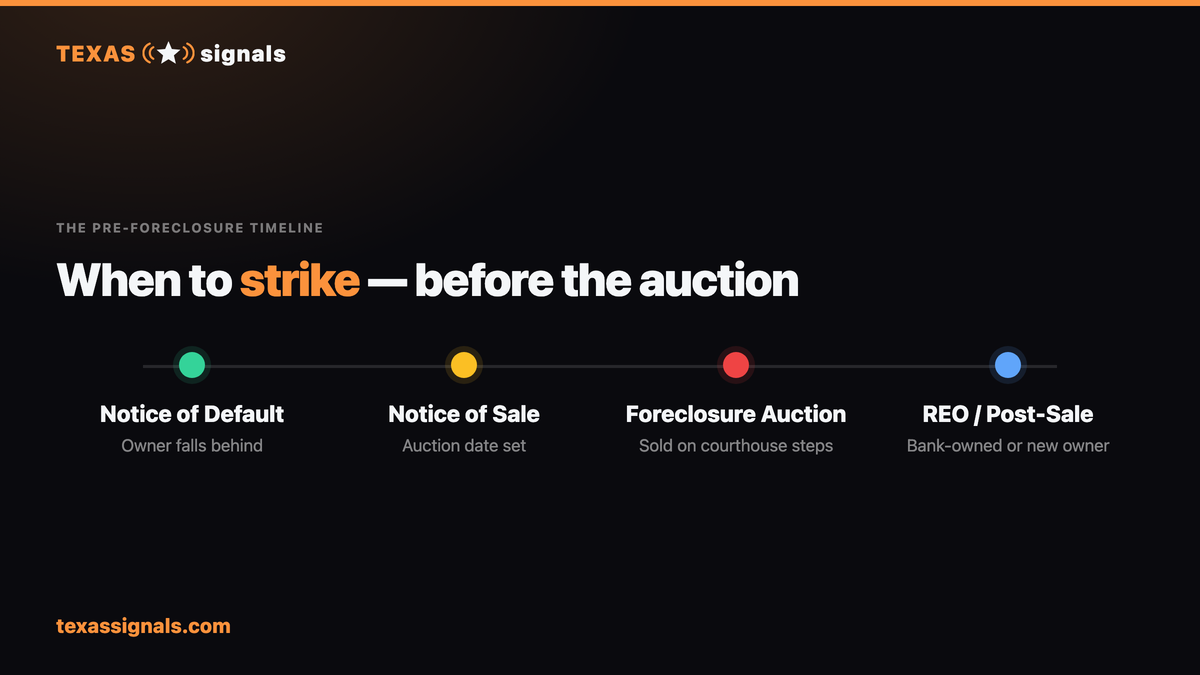

The Texas Pre-Foreclosure Timeline

Understanding the timeline is crucial because it tells you how much runway you have to reach a homeowner before the property goes to auction. Here's how it typically unfolds in Texas:

Phase 1: Missed Payments (Day 1–90)

The borrower misses one, two, then three mortgage payments. The lender sends notices and makes phone calls. Nothing is public yet — you won't see this in any database. The homeowner is stressed but still has options.

Phase 2: Notice of Default / Lis Pendens Filed (Day 60–120)

This is where it gets real. The lender (or their attorney) files paperwork with the county. In Texas, for non-judicial foreclosures, they send a Notice of Default and Intent to Accelerate. For judicial foreclosures, they file a lawsuit and a lis pendens.

This is the moment the information becomes public. This is what Texas Signals scrapes from county records every day.

Phase 3: Notice of Trustee's Sale (At Least 21 Days Before Auction)

Texas law requires the lender to post a Notice of Trustee's Sale at least 21 days before the auction date. The notice must be filed with the county clerk and posted at the courthouse door.

Phase 4: Auction Day (First Tuesday of the Month)

In Texas, foreclosure auctions happen on the first Tuesday of every month, between 10 AM and 4 PM, at the county courthouse. The property is sold to the highest bidder — which is often the bank itself (these become REO properties).

Source: Texas Signals — aggregate county data.

How Investors Use Lis Pendens Data

So you've got access to lis pendens filings — thousands of them across Texas. Now what? Here's the practical playbook:

Step 1: Filter for Equity

Not every pre-foreclosure is a deal. The key metric is equity — the gap between what the property is worth and what's owed on the mortgage. If a homeowner owes $280K on a property worth $350K, there's $70K of equity to work with. That's a potential deal.

If they're underwater (owe more than it's worth), you're looking at a short sale situation, which is a completely different — and much slower — process.

Step 2: Assess the Timeline

Properties with auctions 60+ days out give you time to build rapport with the homeowner. Properties with auctions in 14 days? The homeowner is either already working with someone or they've checked out emotionally. Adjust your approach accordingly.

Step 3: Skip Trace and Make Contact

Use the property address to find the homeowner's phone number, email, and mailing address. This is called "skip tracing." Then reach out — respectfully. These are people going through one of the hardest moments of their lives.

Step 4: Run Your Numbers

If you get a conversation going, you need to know your numbers cold:

•After Repair Value (ARV) — what the property would sell for in good condition

•Repair costs — get this from a contractor, not from your gut

•Existing liens — mortgage balance, tax liens, mechanic's liens, HOA dues

•Your offer — ARV minus repairs minus your profit minus holding costs

Step 5: Present the Offer

If the numbers work, present a fair offer. Be transparent about how you calculated it. Homeowners in pre-foreclosure often appreciate honesty more than a hard sell.

Why Early Access Matters

Here's the thing about lis pendens data: it's a leading indicator. By the time a property shows up on the MLS as a foreclosure, bank-owned, or REO property, dozens of investors are already competing for it. The margins shrink. The deals get worse.

But when you're working from lis pendens data — fresh filings from the county clerk's office — you're reaching homeowners 4 to 8 weeks before most investors even know the property is in trouble.

That head start is worth everything in a competitive market like Texas.

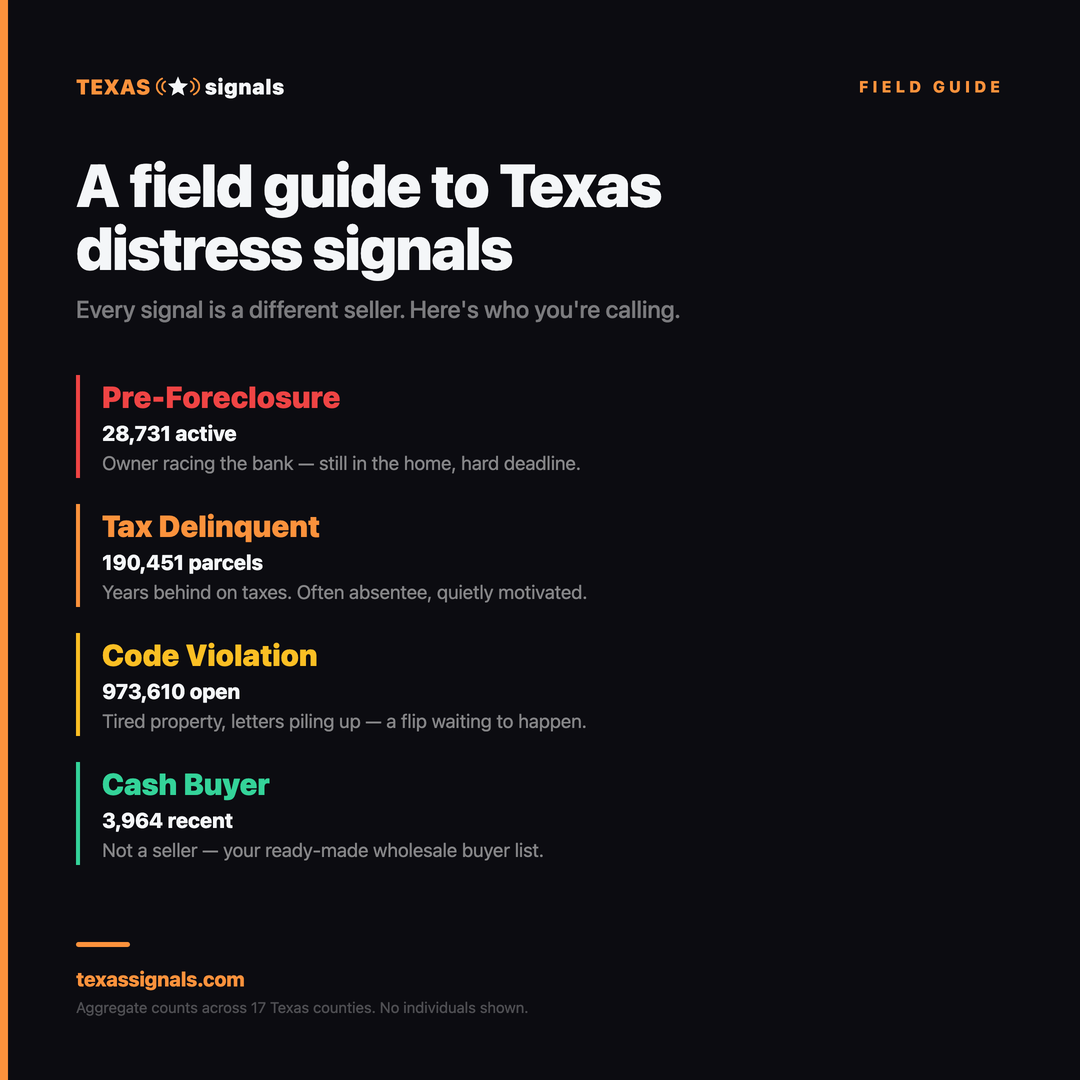

Lis Pendens vs. Other Pre-Foreclosure Signals

It's worth understanding how lis pendens fits into the broader landscape of distress signals:

•Lis Pendens — earliest public notice. Gives you the most runway.

•Notice of Default — similar timing, often filed alongside lis pendens. Some counties use one, some use both.

•Notice of Trustee's Sale — later stage. Auction is imminent (21+ days). Less time to work the deal but higher motivation from the homeowner.

•Tax Delinquency — different type of distress. The homeowner isn't necessarily behind on their mortgage, but they are behind on property taxes. Can compound with a lis pendens.

•Code Violations — property maintenance issues. Often correlate with financial distress but aren't a foreclosure signal on their own.

Texas Signals' Intelligence Score combines all of these signals. A property with a lis pendens AND tax delinquency AND code violations scores significantly higher than one with just a lis pendens alone — because multiple overlapping signals mean the owner is facing pressure from every direction.

Common Mistakes to Avoid

1.Treating every lis pendens as a deal — Many get resolved. Borrowers cure their default, modify their loan, or work out a forbearance. A lis pendens is a lead, not a guaranteed deal.

2.Being aggressive or insensitive — These homeowners are struggling. Aggressive tactics backfire and can get you reported.

3.Ignoring the timeline — A lis pendens from 6 months ago with no auction date might mean the case was dismissed. Check for updated filings.

4.Not verifying the debt — The lis pendens tells you there's a lawsuit, but it doesn't tell you the full picture. There could be second mortgages, tax liens, or other encumbrances you don't see.

5.Skipping title research — Always run a preliminary title search before making an offer. The lis pendens might be the least of your concerns if there are three other liens on the property.

Bottom Line

A lis pendens is the earliest public signal that a property is heading toward foreclosure. For investors, it represents a window of opportunity — a chance to reach motivated sellers before the broader market catches on.

The key is combining early data access (like Texas Signals' daily county scraping) with a respectful, well-prepared approach to homeowner outreach. Lead with empathy, know your numbers, and move with appropriate speed.

The investors who consistently find deals in pre-foreclosure aren't the ones with the most aggressive marketing. They're the ones who show up first with a genuine willingness to help.

Source: Texas Signals — aggregate county data.