Texas Forecloses Fast

Most states require a lender to go through the court system to foreclose on a property. This judicial process can take 12–36 months, giving homeowners a long window to negotiate, sell, or delay.

Texas is different. Texas law allows non-judicial foreclosure, which means a lender can foreclose without filing a lawsuit or getting a judge's approval. The entire process — from first missed payment to completed foreclosure sale — can take as few as 60–90 days under the right conditions.

That speed has significant implications for investors. It means the window to reach a pre-foreclosure homeowner and structure a deal is narrow. It means the data lag problem discussed in [Why National Data Tools Miss the Newest Texas Investors](/blog/why-national-data-tools-miss-newest-texas-investors) isn't just a minor inconvenience — it can eliminate your entire opportunity window.

Understanding the Texas foreclosure process precisely is a prerequisite for working pre-foreclosure leads effectively.

Source: Texas Signals — aggregate county data.

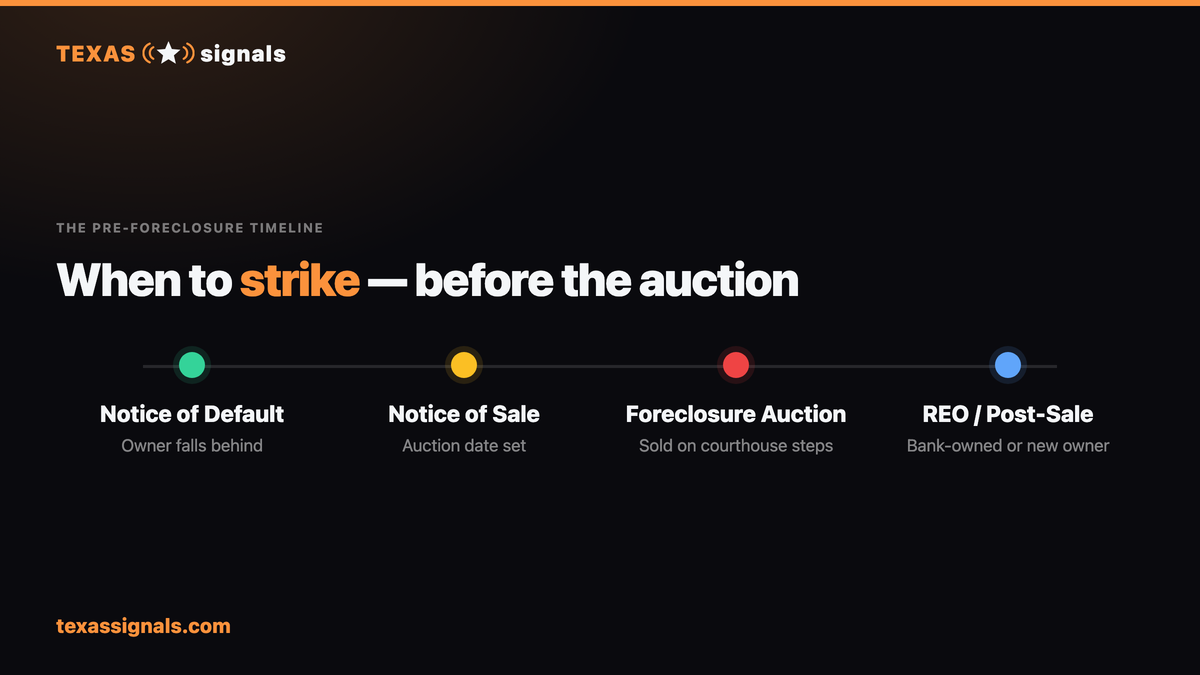

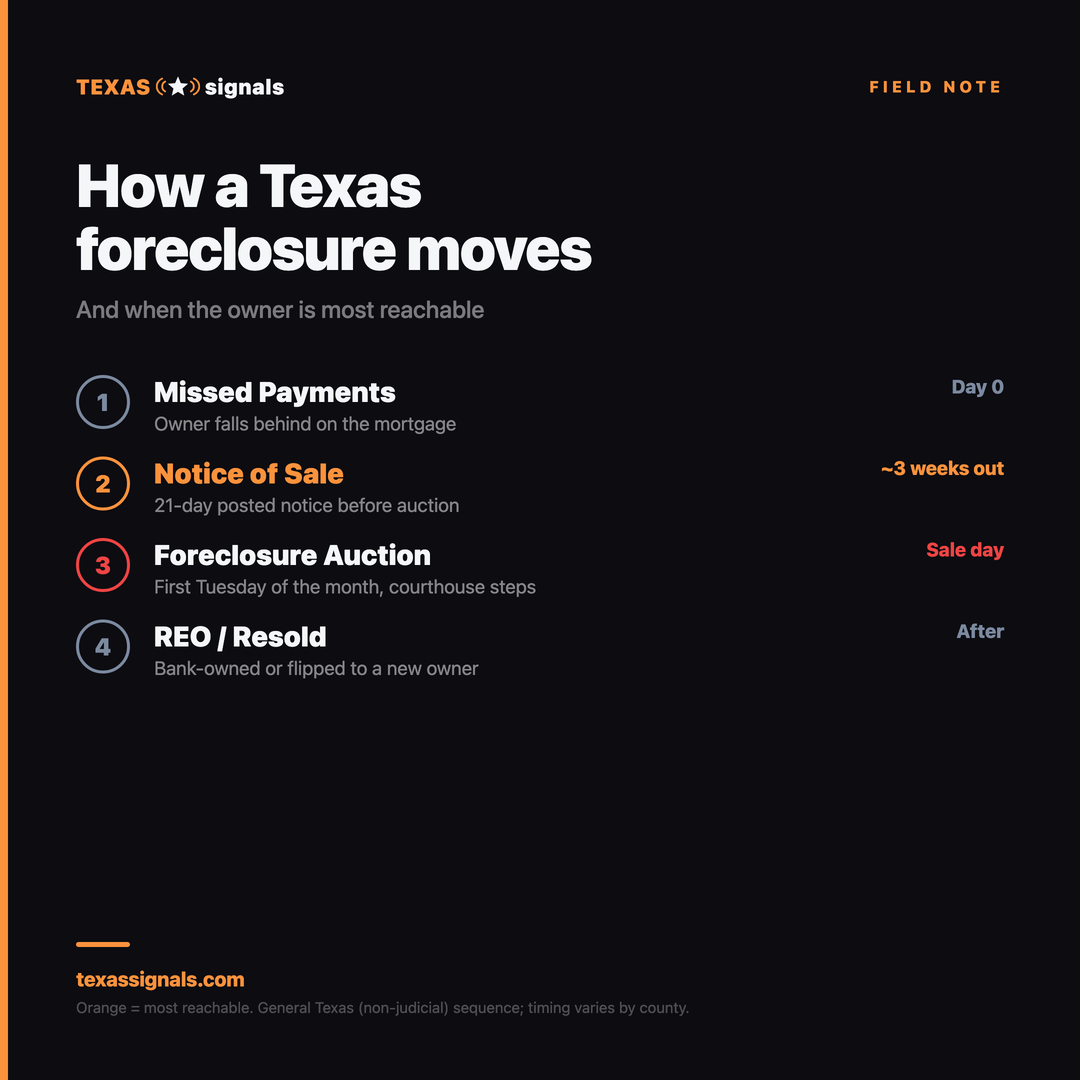

The Texas Non-Judicial Foreclosure Timeline

Stage 1: Default (Day 1 – Day 30+)

A default occurs when a borrower misses a mortgage payment. Most loan contracts include a grace period — typically 10–15 days — before a payment is officially late. After the grace period, the lender can charge a late fee and begin internal collections efforts.

A single missed payment does not trigger foreclosure. Most lenders will not initiate formal proceedings until a borrower is 30–90 days past due, depending on the lender's internal policies and the loan type. During this stage, the default is between the borrower and the servicer — it has not yet appeared in public records.

Stage 2: Notice of Default / Acceleration Letter (Day 30 – Day 60)

When a lender decides to begin formal foreclosure proceedings, they send the borrower a Notice of Default (sometimes called a demand letter or acceleration letter). This notice:

•States the amount of arrears required to cure the default

•Gives the borrower a period to reinstate (catch up on payments) — typically 30 days

•Advises that failure to cure will result in acceleration of the full loan balance

This notice is sent to the borrower but is not yet a public record. The lender is required under Texas law (Texas Property Code Section 51.002) to give the borrower at least 20 days' notice before posting the property for foreclosure sale.

Stage 3: Notice of Sale Posted (Day 60 – Day 90)

At least 21 days before the scheduled foreclosure sale, the lender must:

1.Post a Notice of Sale at the courthouse door of the county where the property is located

2.File the Notice of Sale with the county clerk (this creates the public record)

3.Mail a copy of the Notice to the borrower at their last known address

This is the moment the foreclosure enters public records. Texas Signals monitors county clerk filings and adds properties to our pre-foreclosure feed at this stage — typically within days of the filing.

Stage 4: Foreclosure Sale (First Tuesday of the Month)

Texas law requires that foreclosure sales occur on the first Tuesday of each month at the courthouse steps of the county where the property is located. The sale is conducted by a trustee — typically an attorney appointed by the lender.

At the sale:

•The lender's representative opens with a credit bid equal to the outstanding loan balance

•Third-party bidders may bid above the opening bid

•If no third party bids higher than the lender's credit bid, the property is taken back as REO (Real Estate Owned)

•If a third party wins, they take the property subject to any senior liens

The moment the trustee's deed is recorded, the former owner's interest in the property is extinguished. The previous owner has no redemption right in Texas — unlike in some other states, once the sale is complete, it is complete.

Stage 5: Deficiency (Post-Sale)

If the foreclosure sale price is less than the outstanding loan balance, the lender may pursue the former owner for a deficiency judgment. Texas has some deficiency protections: the lender must file for a deficiency within two years of the sale, and the deficiency amount is limited to the difference between the outstanding loan balance and the fair market value of the property (not the sale price, if lower).

Key Texas Foreclosure Law Provisions

Texas Property Code Section 51.002 governs non-judicial foreclosures. Key provisions:

•At least 20 days' written notice to borrower before posting for sale

•At least 21 days' public notice (courthouse posting + county clerk filing + certified mail) before the sale

•Sales occur only on the first Tuesday of each month between 10:00 AM and 4:00 PM

Homestead protections: Texas has strong homestead protections that limit the types of debt that can trigger non-judicial foreclosure on a primary residence. Voluntary liens (mortgages, HELOCs) can foreclose non-judicially. Judgment creditors generally cannot — they must foreclose judicially, which is slower.

HOA foreclosures: Homeowner associations in Texas can foreclose for unpaid assessments under certain conditions. HOA foreclosures follow a different statutory process and can move quickly on investment properties.

When to Approach the Owner

The optimal contact window is between the Notice of Default (when the lender first demands cure) and the Notice of Sale posting. During this window:

•The homeowner knows they are in serious trouble

•The situation is not yet fully public

•The homeowner still has meaningful options (reinstatement, sale, short sale, deed-in-lieu)

•The timeline is not yet at crisis level — you have space for a real conversation

Once the Notice of Sale is posted:

•The timeline compresses to 21+ days

•Every investor with data access is now competing for the same lead

•The homeowner's options narrow — reinstatement requires a larger payment, short sale requires lender approval and takes longer than 21 days

The Investor's Role in This Process

Pre-foreclosure investing is not predatory when done right. A homeowner who is 60 days behind and facing foreclosure genuinely needs options. Foreclosure damages their credit severely, leaves them with nothing (no equity extraction), and can have lasting financial consequences.

A cash offer that closes before the foreclosure sale:

•Lets them extract whatever equity exists above the loan payoff

•Stops the credit damage of a completed foreclosure

•Gives them certainty and control over their timeline

•Eliminates the stress of the foreclosure process

The investor who reaches them early, is honest about what they're doing, and makes a fair offer does the homeowner a genuine service. The investor who shows up at the courthouse on sale day with a lowball bid does not.

For outreach scripts tailored specifically to pre-foreclosure conversations, see [Outreach Scripts for Every Distress Signal](/blog/outreach-scripts-distressed-properties).

Source: Texas Signals — aggregate county data.

To see current pre-foreclosure filings in your target county, visit [Texas Signals pricing](/pricing).

See your county's data — [start your 7-day free trial](https://texassignals.com/trial).