Texas Is a Non-Judicial Foreclosure State — and That Changes Everything

Source: Texas Signals — aggregate county data.

If you're coming from a state like New York or Florida, you need to reset your assumptions. In those states, foreclosure goes through the court system and can take 12–36 months. In Texas, the most common path is non-judicial foreclosure, which means the lender doesn't need a judge's permission to sell your house.

The result? Texas foreclosures move fast. The legal minimum from first notice to auction is just 41 days. In practice, most take 60–180 days, but the speed is real.

The Complete Timeline

Source: Texas Signals — aggregate county data.

Let's walk through every phase, from the first missed payment to auction day. I'll include approximate timing, but remember — every situation is different.

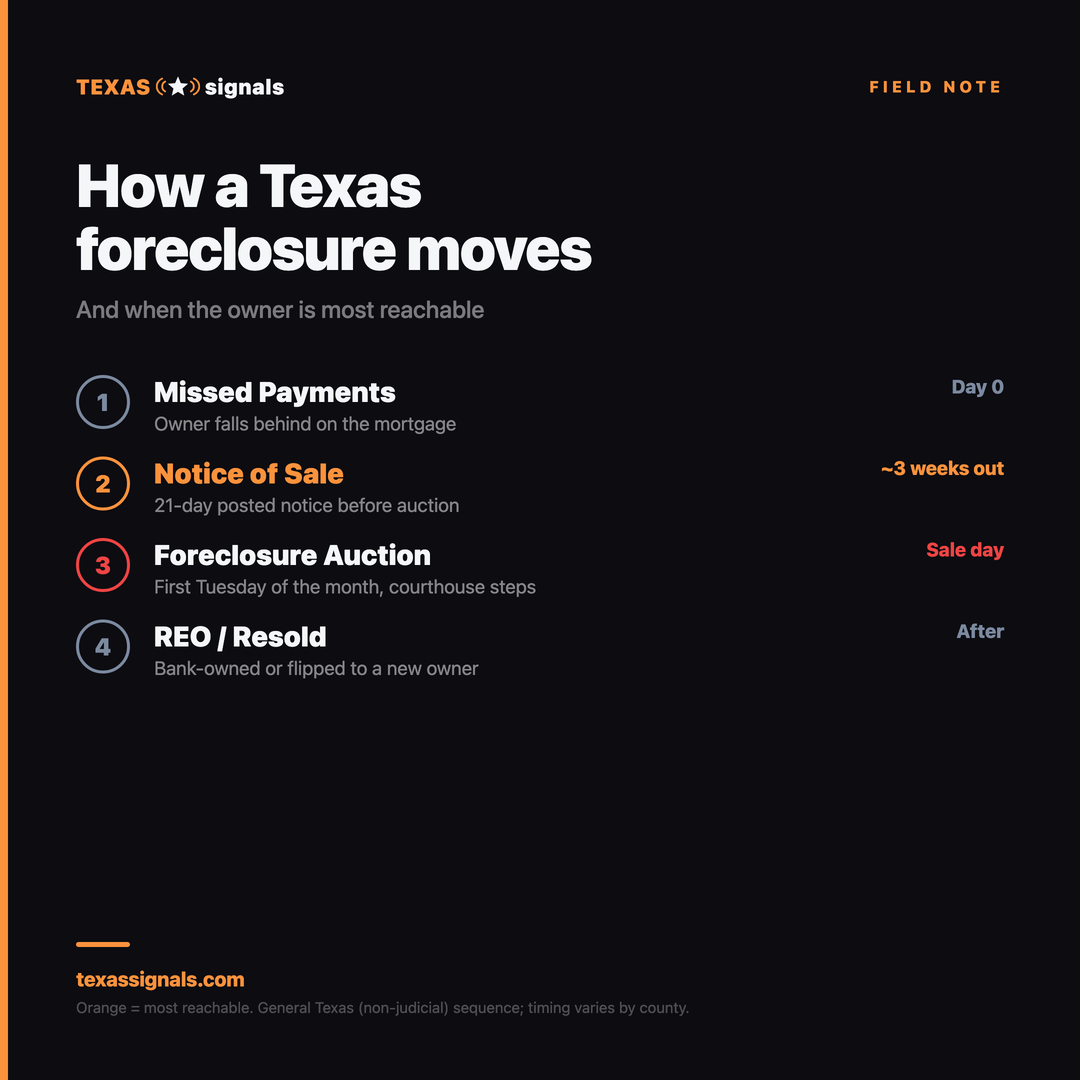

Month 1-3: Missed Payments (Not Yet Public)

The borrower misses their first mortgage payment. The lender sends a late notice (usually after a 15-day grace period). After 30 days past due, it hits the borrower's credit report.

During months 2 and 3, the lender's loss mitigation department reaches out with phone calls, letters, and emails. They'll often offer options:

•Forbearance — temporarily reduced or paused payments

•Loan modification — permanently restructured terms

•Repayment plan — catch up over time while staying current going forward

Most borrowers who fall behind do catch up. Only a fraction of missed payments become actual foreclosures.

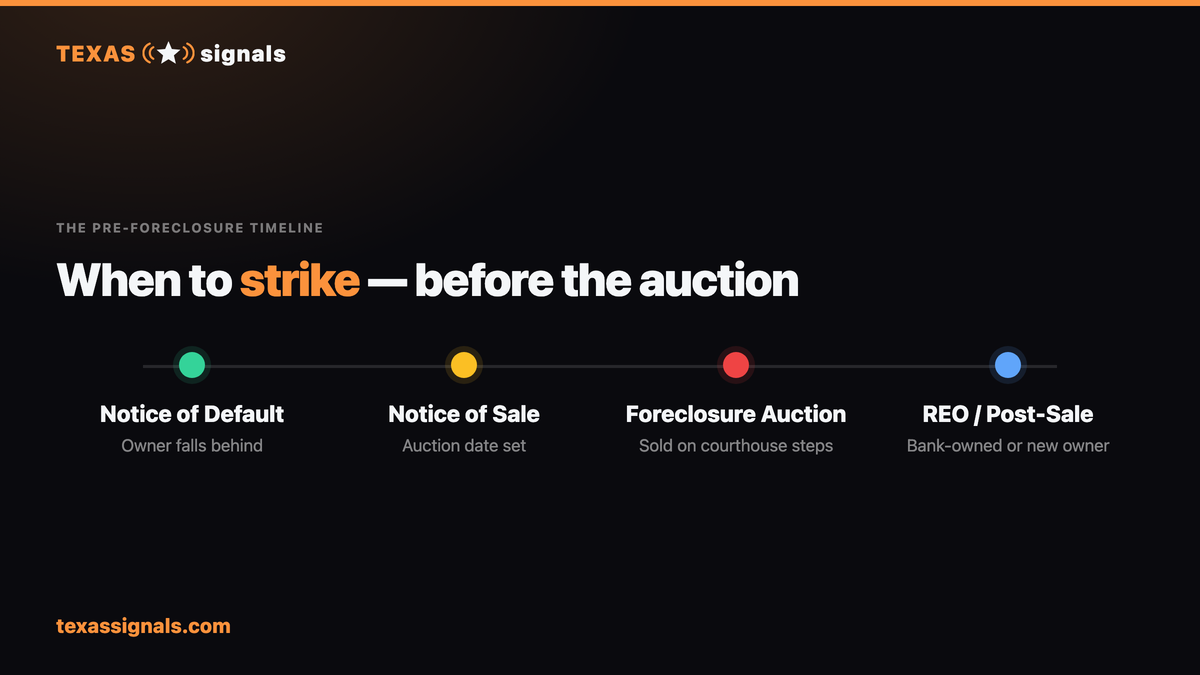

Day 0: Notice of Default and Intent to Accelerate

When the lender decides to proceed with foreclosure, they must send the borrower a written notice that:

•States the borrower is in default

•Describes what the borrower must do to cure the default

•Gives the borrower at least 20 days to cure before acceleration

This notice must be sent by certified mail. This is often (though not always) the point where the filing becomes part of the public record.

Day 21+: Notice of Sale Filed

After the 20-day cure period expires (assuming the borrower didn't cure), the lender can post a Notice of Trustee's Sale. Texas law requires:

1.Filed with the county clerk in the county where the property is located

2.Mailed to the borrower by certified mail at least 21 days before the sale date

3.Posted at the courthouse door (or the area designated by the county commissioners) at least 21 days before the sale

The sale must occur on the first Tuesday of a calendar month, between 10:00 AM and 4:00 PM, at the location designated by the county commissioners.

Auction Day: First Tuesday of the Month

This is where it all comes to a head. Every county in Texas holds its foreclosure auctions on the same day — the first Tuesday of the month. Here's what happens:

•The substitute trustee (appointed by the lender) conducts the sale

•Bidding starts at the amount owed on the mortgage (plus fees and costs)

•If no one bids higher, the lender takes the property back (it becomes REO — Real Estate Owned)

•The winning bidder pays in cash or cashier's check — no financing at auction

•The trustee executes a Trustee's Deed transferring the property to the winner

Judicial vs. Non-Judicial: What's the Difference?

Texas allows both, but non-judicial is far more common for residential mortgages with a power-of-sale clause (which is virtually all of them).

Non-judicial (most common):

•Faster (41 days minimum)

•No court involvement

•Lender uses the "power of sale" clause in the deed of trust

•No right of redemption after sale

Judicial (less common):

•Goes through the court system

•Takes 6-18 months

•Lender must file a lawsuit and get a judgment

•Used when there's no power-of-sale clause, or when the lender needs a deficiency judgment

•A lis pendens is filed as part of the judicial process

Why This Matters for Investors

The type of foreclosure affects your strategy:

•Non-judicial foreclosures give you less time but more certainty about the auction date. The first Tuesday rule makes scheduling predictable.

•Judicial foreclosures give you more time to work the deal, but the timeline is less predictable because it depends on court schedules.

•Lis pendens filings are your early warning system for judicial foreclosures. For non-judicial, you're watching for Notices of Default and Notices of Sale.

The Investor's Window of Opportunity

Here's the timeline from an investor's perspective:

Window 1: Pre-Default (Best, But Hardest to Find)

Before any public filing. You'd need direct marketing (driving for dollars, mailers) to find these homeowners. No data advantage here.

Window 2: After Default Notice, Before Sale Notice (Sweet Spot)

The homeowner knows they're in trouble. They've received the official notice. They have 20+ days before things escalate. This is where data tools like Texas Signals give you an edge — you see the filing the day it hits public record.

Window 3: After Sale Notice, Before Auction (Urgent)

The auction date is set. The clock is ticking. The homeowner's motivation is highest, but so is the competition. Other investors and real estate attorneys are watching the same notice postings.

Window 4: At Auction (Cash Only)

You're competing against other investors and the bank's opening bid. No inspections, no financing contingencies, limited title research. High risk, but properties can sell below market value.

Window 5: Post-Auction / REO (Competitive)

The bank took the property back. Now it's listed through an asset management company. You're competing with retail buyers, other investors, and you're paying closer to market value.

Key Numbers Every Texas Investor Should Know

•41 days — minimum legal timeline from first notice to auction

•21 days — minimum notice before trustee's sale

•20 days — minimum cure period after Notice of Default

•First Tuesday — every foreclosure auction in Texas happens on this day

•10 AM – 4 PM — auction hours (county-specific within this window)

•$0 redemption period — for non-judicial foreclosures, there is none

•6 months — redemption period for homestead properties in tax foreclosures

•2 years — redemption period for certain agricultural properties in tax foreclosures

What Happens to the Homeowner After Auction?

After a non-judicial foreclosure sale in Texas:

1.The borrower must vacate. The new owner can file for eviction if they don't leave voluntarily.

2.Deficiency judgment — if the property sold for less than what was owed, the lender CAN pursue the borrower for the difference, but they must file a separate lawsuit within 2 years.

3.Credit impact — a foreclosure stays on the borrower's credit report for 7 years.

4.Tax implications — forgiven debt may be taxable income (though there are exceptions).

Bottom Line

Texas foreclosure moves fast. The non-judicial process can wrap up in as little as 41 days, and there's no redemption period after auction. For investors, this creates a narrow but valuable window to identify and reach motivated homeowners.

The investors who win in this market are the ones who get the data first, move quickly but respectfully, and always know their numbers before making an offer.

Source: Texas Signals — aggregate county data.