How Texas Foreclosure Auctions Work

Source: Texas Signals — aggregate county data.

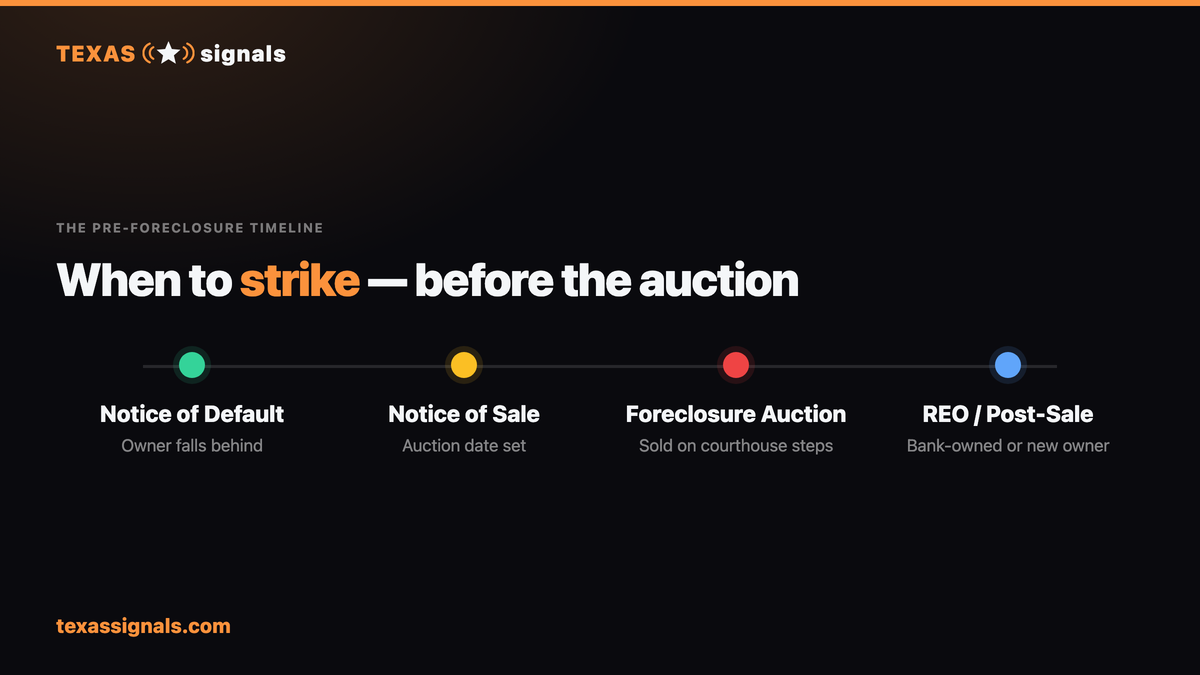

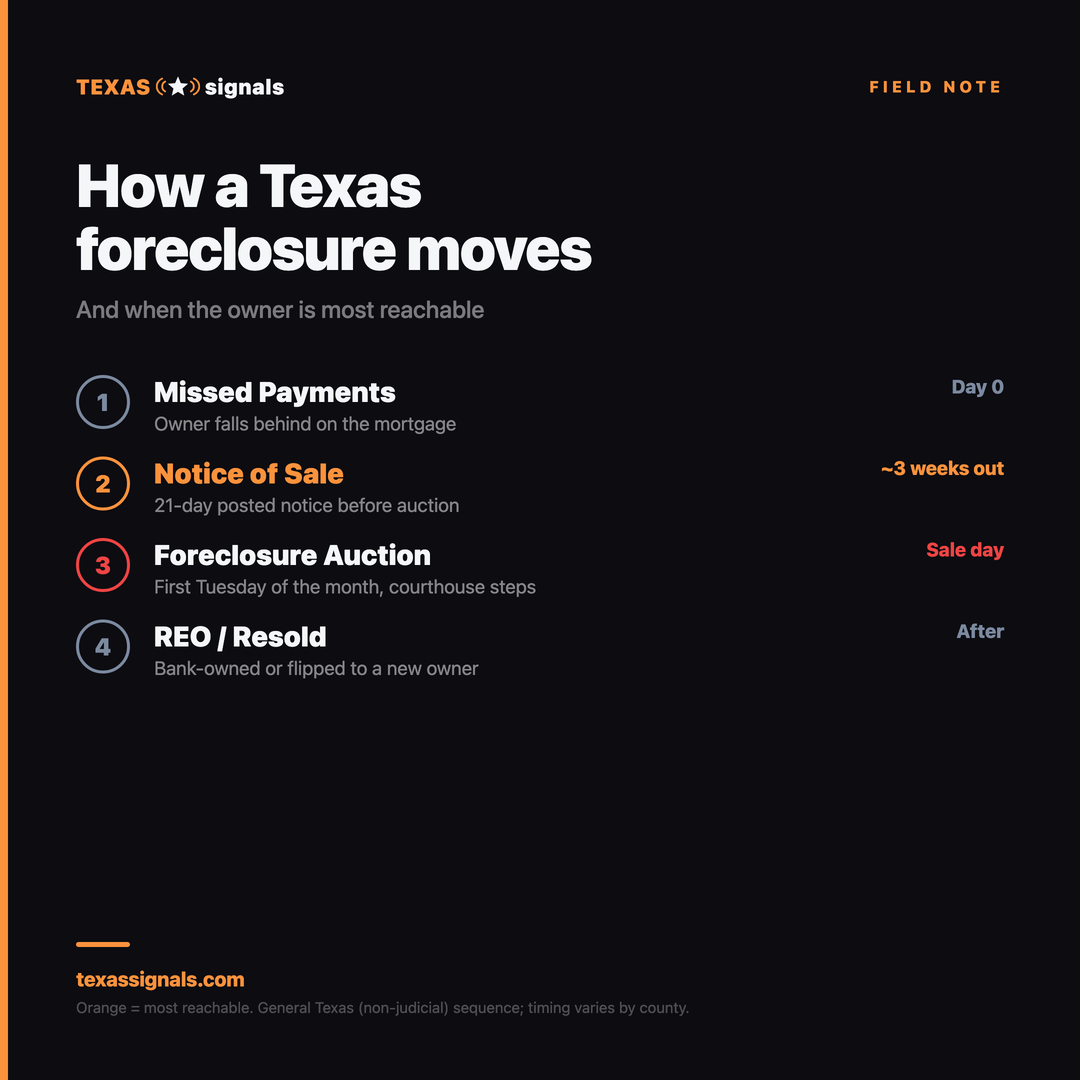

Texas is a non-judicial foreclosure state, meaning lenders can foreclose without going through the court system (with some exceptions). The process follows a defined timeline:

1.Default — Borrower misses payments (typically 3+ months)

2.Notice of Default — Lender sends formal notice, giving 20 days to cure

3.Notice of Sale — Filed with county clerk at least 21 days before auction

4.Auction — First Tuesday of the month, at the county courthouse (or designated location)

5.Trustee's Deed — Winning bidder receives deed; no redemption period for non-homestead properties

Harris County Auction Basics

Harris County conducts foreclosure sales at the Bayou City Event Center on the first Tuesday of each month. Key logistics:

•Time: 10:00 AM - 2:00 PM

•Payment: Cashier's check or cash required at time of sale

•Opening bid: Typically the outstanding loan balance plus fees

•No inspection: You cannot inspect the interior before bidding

•No title insurance: Title is conveyed "as-is"

Pre-Auction Research: The Texas Signals Advantage

The most successful auction buyers do not win on auction day. They win in the weeks before, through research. With 17,680 active pre-foreclosure filings in Harris County, Texas Signals provides the raw data needed to build your research list:

Step 1: Identify Target Properties (4-8 weeks before auction)

Filter pre-foreclosure filings by ZIP code, filing date, and estimated equity. Focus on properties where:

•The filing is at least 60 days old (closer to auction)

•The estimated equity exceeds 20% of current value

•The property is in a neighborhood you know well

Step 2: Drive the Properties (2-4 weeks before auction)

Physically visit each property on your shortlist. Assess exterior condition, neighborhood quality, comparable properties, and occupancy status. This step eliminates 60-70% of candidates.

Step 3: Research Title (1-2 weeks before auction)

Pull a title search for each remaining candidate. Look for:

•IRS liens — Federal tax liens survive foreclosure and transfer to the buyer

•HOA liens — Super-priority HOA liens may survive foreclosure

•Senior liens — If the foreclosing lien is a second mortgage, the first mortgage survives

•Judgment liens — May or may not survive depending on recording date

Step 4: Calculate Maximum Bid

Max bid = Estimated ARV x 0.75 - Estimated Repairs - Holding Costs - Profit Target

Example:

•ARV: $350,000

•75% of ARV: $262,500

•Repairs: $45,000

•Holding costs (6 months): $12,000

•Profit target: $40,000

•Maximum bid: $165,500

Step 5: Attend and Bid

Arrive early. Bring multiple cashier's checks in different denominations. Stick to your maximum bid. The most expensive mistake in auction investing is emotional bidding.

Risks of Foreclosure Auction Buying

1. Occupancy

The property may be occupied by the former owner, a tenant, or a squatter. Texas law requires formal eviction proceedings, which can take 30-60 days.

2. Condition Unknown

You cannot inspect the interior. Assume the worst-case repair scenario and add 20% contingency.

3. Title Defects

While the trustee's deed conveys the property, title defects can survive. Budget for a post-purchase quiet title action if needed ($2,000-$5,000 in legal fees).

4. Redemption Rights

For homestead properties, the previous owner has a 2-year redemption right. They can reclaim the property by paying you the purchase price plus 25% (year 1) or 50% (year 2) premium.

The Pre-Auction Alternative

Many experienced investors prefer to contact homeowners before the auction. The pre-foreclosure window (60-180 days before sale) allows for negotiated purchases at below-market prices without the risks of auction buying. Texas Signals' pre-foreclosure tracking makes this approach systematic rather than relying on driving neighborhoods.

Source: Texas Signals — aggregate county data.

Source: Texas Signals — aggregate county data.

Texas Signals tracks every pre-foreclosure filing and foreclosure auction in Harris County. Get daily updates at [texassignals.com](/).